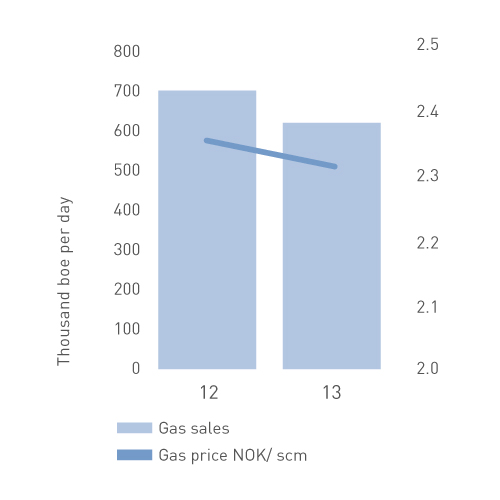

Norwegian gas exports fell by five per cent from a record 2012 level. High gas prices in Asia during 2013 again meant that

liquefied natural gas (LNG) originally intended for the European market was sent instead to eastern markets. Russia functioned as the swing producer for Europe, and increased its gas deliveries there by roughly 16 per cent in 2013. Part of the gas volume sold to Europe is priced in accordance with market quotations which reflect the balance between supply and demand (spot pricing). Prices in the European gas market were somewhat lower than in 2012, but still move at a relatively high level.

The average gas price for the SDFI portfolio in 2013 was NOK 2.31 per scm, compared with NOK 2.35 the year before.

Petoro has worked to ensure maximum value creation for the gas portfolio. The company is concerned to ensure that available gas is sold in the market at the highest possible price, and that the flexibility of production plants and transport capacity is exploited to optimise deliveries.

Petoro also monitored and assured itself that petroleum sales to Statoil’s own facilities are made at their market-based value. In addition, checks were made to ensure that the SDFI was being charged an equitable share of costs and received its equitable share of revenues.