The SDFI was established with effect from 1985. Under this arrangement, the state participates as a direct investor in petroleum operations on the Norwegian continental shelf (NCS) so that the Treasury receives revenues and meets expenses associated with the SDFI’s participatory interests directly and outside the regular system for taxing petroleum revenues. Petoro acts as the licensee for the state’s participatory interests in production licences, fields, pipelines and land-based facilities, and manages the portfolio on the basis of sound business principles.

External trends

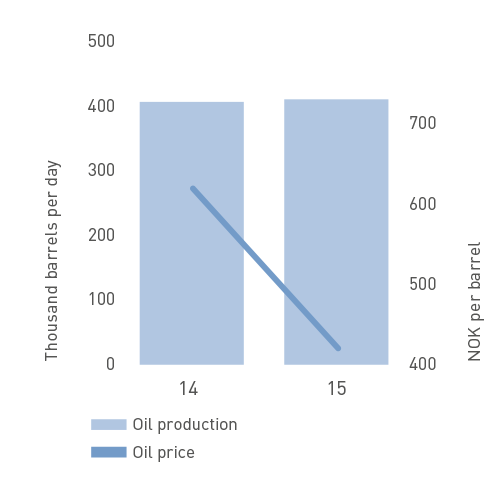

Global economic growth was moderate in 2015 and rather weaker than expected. Moderate growth combined with a substantial decline in crude prices have helped to boost demand for oil. But production has increased by more than demand, and resulted in a weaker market balance and stronger pressure on crude prices. The inventory build-up was substantial, and oil storage had reached a record level by 31 December. In November, Opec reaffirmed its 2014 decision to maintain an unchanged level of production. Brent Blend declined over the year to USD 37 per barrel, virtually half its top price of USD 66 in May 2015. Market volatility was also high. The average price for the portfolio came to USD 53 per barrel, compared with USD 99 in 2014. A weaker exchange rate reduced the revenue decline in Norwegian kroner, where the average price was NOK 420 per barrel – down by NOK 197 from the year before.

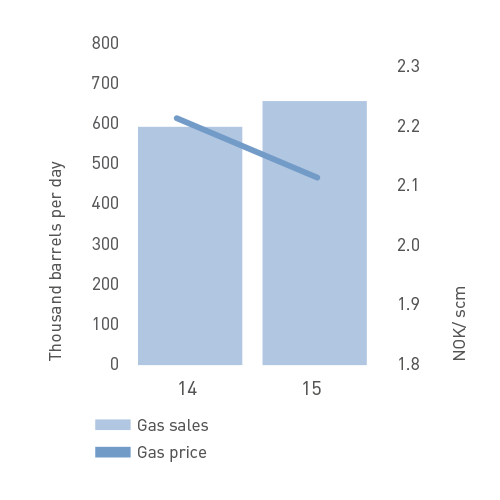

European demand for natural gas rose somewhat in 2015, in part because the winter was colder than in 2014. But gas is still subject to increased competition from renewable energy, coal, and the consequences of improved energy efficiency. Europe’s own gas production fell further in 2015, reinforced by lower Dutch output as a result of technical challenges in the Groningen field. This decline was offset by increased imports from Russia and Norway and as liquefied natural gas (LNG). Norway’s gas exports set a record in 2015. Robust supplies and the fall in the cost of oil reduced gas prices over the year, but the weaker Norwegian krone offset the effect of this decline. The average gas price achieved for the portfolio was NOK 2.14 per scm in 2015, compared with NOK 2.23 in 2014.

Agreement was reached at the summit in Paris during December 2015 on an international climate agreement with a clear ambition of reducing global greenhouse gas emissions. That helps to increase uncertainty on the demand side.

The petroleum sector is also under considerable pressure to reduce total emissions from oil and gas production, which means the industry must develop low-emission solutions and enhance energy efficiency.

Substantial changes are under way in the petroleum industry. Great uncertainty prevails over future oil price developments, profitability and competitiveness. The sector is characterised both in Norway and internationally by investment cut-backs and downscaling of the level of activity, which are reflected by the reduced scope of new projects.

Commitment to cost reductions and greater efficiency increased during 2014 and 2015. The need to secure a rapid improvement in cash flow was directed moreover at reduced activity, cost/benefit assessment of measures, simplification and standardisation of solutions and work processes, improved planning and renegotiation of contractual rates. The measures initiated have had a big impact in certain areas, such as drilling and field costs. A substantial potential still exists for further efficiency improvements through innovative technology, better collaboration between players and new operating models. Such measures will take longer to identify and implement, since they call for substantial changes in the way the industry works.

Current efficiency improvements and initiatives to reduce the level of costs in the industry are crucial for improving profitability both in the near future and in the long term. Greater emphasis on financial robustness challenges profitability and the choice of solutions in projects. The scope and speed of this improvement work affects Petoro’s opportunities to realise the value potential of the portfolio for both mature fields and possible new field developments.

Summary of SDFI results

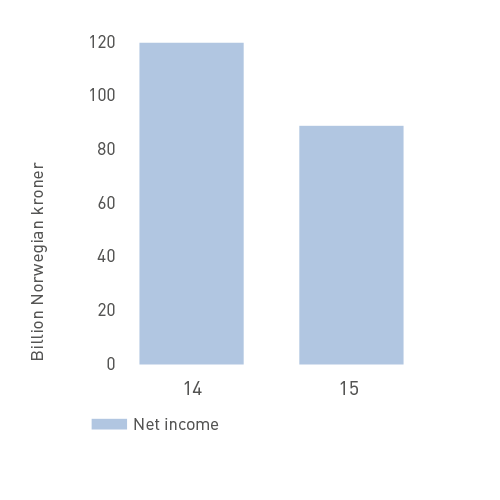

Financial results for the SDFI in 2015 were strong despite the significant reduction in commodity prices from the year before. Net income in 2015 came to NOK 89 billion, down by NOK 31 billion from 2014. Cash flow to the government was NOK 94 billion, 15 per cent lower than the year before despite a halving of oil prices in US dollars from 2014 to 2015.

A weaker exchange rate against the US dollar helped to maintain revenues measured in Norwegian kroner. Gas revenues represent an increasingly important share of SDFI income. Relatively stable prices combined with higher sales maintained good gas earnings. Total production averaged 1 068 000 barrels of oil equivalent per day (boe/d), about seven per cent higher than in 2014. That primarily reflected improved production efficiency (PE) and the completion of more wells. Some gas production was also transferred from 2014 to 2015. Sales for the year corresponded to production.

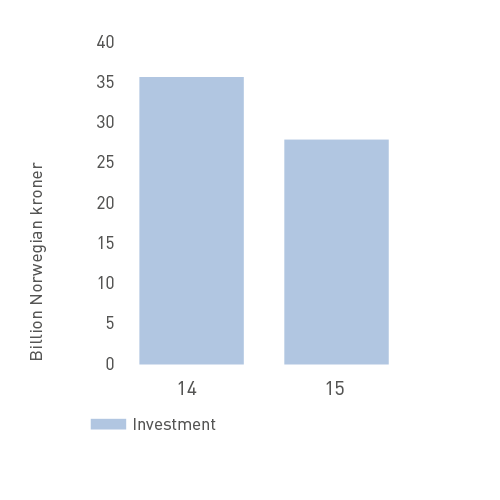

Investment for 2015 totalled NOK 28 billion, down by NOK 8 billion from the year before. This decline was in line with expectations and primarily reflected lower capital spending on development and operations as a result of reduced project activities.

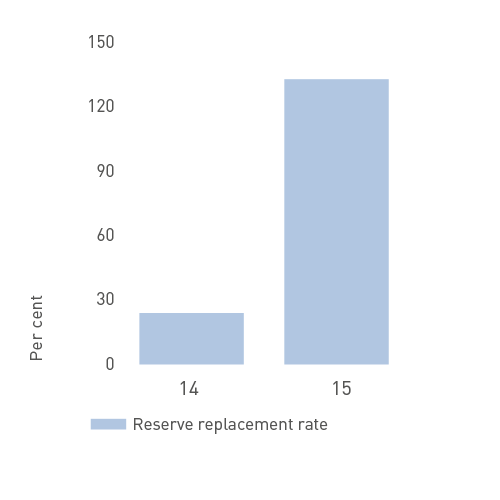

At 31 December 2015, the portfolio’s expected remaining oil, condensate, NGL and gas reserves comprised 6 276 million boe. That was up by 130 million boe from the end of 2014 when account is taken of production for the year and new reserves. The increase in the portfolio’s reserves is attributable almost entirely to the decision to develop Johan Sverdrup.

The book value of assets totalled NOK 248 billion at 31 December 2015. These assets comprise operating facilities related to field installations, pipelines and land-based plants, as well as current debtors. Assets have been assessed for impairment in light of the low oil prices. Impairment charges of about NOK 5 billion were taken in 2015. Equity at 31 December amounted to NOK 161.5 billion.

Principal activities in 2015

The portfolio comprised 174 production licences at 31 December, a reduction of eight from 1 January. Participatory interests in 13 production licences were awarded for Petoro to manage through the 2015 awards in predefined areas (APA) in January 2016.

The company’s strategy was last revised in 2013, and its most important elements have been a concentration on mature fields, field development and the far north. A decision to initiate a new strategy process was taken by the board in the autumn of 2015, and plans call for this work to be completed during the first half of 2016.

Output from the mature oil fields continues to dominate production in the portfolio. Troll, Åsgard, Oseberg, Heidrun, Snorre and Gullfaks accounted for about 60 per cent of total liquids production.

Just over 70 per cent of gas output came from Troll, Ormen Lange and Åsgard. New capacity was introduced in 2015 when Åsgard subsea compression, Valemon, Oseberg Delta 2, Troll gas compression and Eldfisk II came on stream. In addition, Gullfaks wet gas compression was installed during the year but did not begin operation.

In line with the strategy, work continued in 2015 on realising the reserve base and supplementary resources in the mature fields, with special commitments made to Snorre, Heidrun and Oseberg.

With today’s high level of costs and low raw material prices, companies on the Norwegian continental shelf (NCS) are devoting great attention to improving profitability and cash flow. Petoro is finding that short-term considerations wrestle with longer-term concerns. This makes it challenging to secure the necessary decisions which are important for long-term value creation, and not least to ensure that these are taken at the right time.

Petoro is an active driving force on the Snorre 2040 project, and contributed through its own work in 2015 to strengthening the reserve potential for a major new development solution. Challenging profitability prompted yet another postponement of the decision on continuation to the fourth quarter of 2016 and the introduction of a new concept based on subsea solutions as an alternative to a new Snorre C platform. Petoro has made its own assessments of the opportunities offered by a new concept for securing a realisation of the greatest possible value from further development of the field. Current plans call for an investment decision in 2017 and a start to production in 2021. The new solution makes it possible to realise Petoro’s ambition.

Through its own simulation studies on Heidrun, Petoro has increased understanding of the reservoir in the northern parts of this field where the potential for improved recovery is greatest. This work has helped to reduce uncertainty and strengthen the reservoir potential for the Heidrun subsea extension project, with a choice of concept planned for early 2017.

The contribution made by Petoro to Oseberg in 2015 was directed at improving the drainage strategy and ensuring robustness in the Oseberg future development project. A decision has been taken on a new simple and unstaffed wellhead platform as the first stage of the Oseberg Vestflanken 2 project. This innovative solution is entirely in line with Petoro’s view, and could open new opportunities for further field development. A plan for development and operation (PDO) was submitted in December 2015, with production planned to begin in 2018.

Petoro’s commitment to Johan Sverdrup in 2015 was linked to an integrated development of the field and to ensuring robust procurement strategies for its first stage. The PDO for phase one was submitted in February 2015 with a development solution which, in line with Petoro’s view, lays the basis for good long-term value creation. Where future phases are concerned, an expansion of production capacity with a new platform at the field centre will provide the greatest long-term value creation. Petoro worked in 2015 to ensure that this structure will be as cost-effective as possible, and secured acceptance for further maturation of the concept up to decision gate 2 (DG2) in the autumn of 2016.

The company continued its own analysis work on the value potential of advanced improved recovery from Johan Sverdrup, and proposed solutions in this area. The licensees are planning a pilot project for such recovery after phase one has come on stream. Petoro has also sought to establish a robust basis for electricity supply capacity which ensures sufficient power in the long term.

Extensive work related to the unitisation of Johan Sverdrup was completed by Petoro during 2015, and a negotiated unitisation agreement was presented to the government for determination of the final terms in conjunction with the submission of the PDO in February 2015. The Ministry of Petroleum and Energy (MPE) decided on a division of Johan Sverdrup on 1 July 2015 which gave the SDFI a 17.36 per cent holding in the field.

In the far north, Petoro’s attention has been concentrated on the portfolio in Barents Sea South with the emphasis on Snøhvit, Johan Castberg and the Hoop area.

Where the Johan Castberg project is concerned, Petoro continued to focus during 2015 on improving profitability and enhancing the robustness of alternative concepts assessed by the licensees. A decision on continuation (DG2) was postponed in February 2015 to the third quarter of 2016, and the licensees opted in December 2015 for a production ship as the development concept. Petoro has contributed to ensuring that the chosen solution has sufficient processing capacity to provide tie-back opportunities for possible supplementary resources in the area.

Petoro continued to direct the industry’s attention during 2015 towards the need to speed up the pace of drilling through improved efficiency and cost reductions in the drilling and well service area. The company has followed up progress with drilling speed from 10 fixed installations on five fields over several years, and has seen a doubling in the number of wells there over the past two years along with a halving in drilling costs for each well. This reflects a combination of more efficient drilling, simplification of well design and increased availability of drilling facilities.

Growing attention was paid by Petoro in 2015 to the need for improved efficiency also in development, operation and maintenance. The company worked to ensure that the measures adopted are sustainable in both short and long terms, and involve a genuine enhancement in efficiency rather than simply a reduction in activity. The aim is to increase competitiveness and thereby ensure the profitability of investment in mature fields and new developments. Petoro observed that field costs related to some important fields were also substantially reduced from the 2013 level during 2015. In addition, restructuring efforts by the operators contributed to big reductions in operational modifications. Achieving further cost reductions is expected to be more challenging.

Four PDOs were approved by the government in 2015, covering Gullfaks Rimfaksdalen, Johan Sverdrup phase one, Maria and Gullfaks Shetland/Lista. The PDO for Oseberg Vestflanken 2 was adopted by the licensees and submitted to the MPE in December.

Exploration activity on the NCS was high in 2015. Petoro participated in 13 of the 57 exploration wells completed during the year. Seven new but small discoveries were made in the portfolio.

Reserves increased substantially over the year, primarily as a result of the development decision for Johan Sverdrup. The overall rise for the portfolio over the year was 520 million barrels of oil equivalent (boe). A total of 390 million boe was produced in 2015, giving an estimated net reserve replacement rate of 133 per cent. The comparable figure in 2014 was 24 per cent.