The SDFI arrangement was established in 1985. The arrangement entails that the state participates as a direct investor in the petroleum activity on the Norwegian shelf, so that the state receives revenues and incurs costs associated with the SDFI shares. Petoro acts as a licensee for the state’s interests in production licences, fields, pipelines and onshore facilities. As manager of SDFI, Petoro contributed a cash flow of NOK 120 billion in 2018, a significant part of the state’s total revenues from the petroleum activity.

External trends

The Norwegian oil and gas activities operate in a global arena with tough competition for capital and competence. Therefore, maintaining the competitiveness of the shelf will be crucial to the future of the Norwegian petroleum industry.

The Norwegian petroleum industry is now characterised by optimism. Several years of adjustment and efficiency measures, well-assisted by the fact that oil and gas prices stabilised in 2018 at a somewhat higher level than the previous year, give the industry a good starting point for new profitable investments and increased activity. Demand for oil and gas is still increasing, but prices are uncertain and considerable volatility is expected in the time ahead.

Gas makes an increasing contribution towards phasing out coal in several countries, thus substantially reducing greenhouse gas emissions. The Intergovernmental Panel on Climate Change’s (IPCC’s) status report from October describes with even greater clarity than before the consequences of global warming, and that today’s climate measures are far from sufficient. Rapid and far more sweeping measures are called for, and in November, the EU Commission announced its vision for a climate-neutral Europe by 2050. While the greenhouse gas emissions from the Norwegian shelf are low in an international context, it is important that we implement climate measures to further reduce emissions, and thus strengthen competitiveness.

The break-even price for important projects has been substantially reduced in recent years. However, the expected price volatility in the years to come underlines the necessity of further improving the competitiveness and attractiveness of the Norwegian shelf to realise future values. The major effects of adjustment and streamlining we have seen in recent years are levelling off, and we need new measures and new ways of working to achieve further efficiency. At the same time, there is a risk that the cost level will once again rise in line with the increased activity level on the shelf. This can pose a challenge for the shelf’s competitiveness.

In 2018, Equinor presented plans for renewal of the Norwegian shelf. These plans largely coincide with Petoro’s strategy, particularly as regards focus on mature fields, including a significant increase in number of wells, extension of field lifetimes and leverage of existing infrastructure, along with a commitment to digitalisation.

Driven by the need to further improve competitiveness, it is important that we continue the work to reduce uncertainty in reserve estimates, improve efficiency, develop cost-efficient solutions and reduce emissions. Recent years’ strong and rapid development of digital technologies on a global basis are among the most important strategic instruments in most oil and supplier companies. The main challenge when it comes to realising the potential in digitalisation is not primarily technology, but bringing about the changes that are needed in the way we work. Management, culture and work processes are therefore the most important factors.

It is positive that the most important operators and suppliers in the SDFI portfolio work well with digitalisation linked to the areas with the largest commercial significance within both reservoir, drilling and operations. Several successful pilot projects have already yielded good effect. Petoro notes that the operations models are in the process of changing on the operations side through the establishment of onshore operations centres. Activities and personnel within drilling are also being moved onshore. This development is mainly still in an early phase. The industry’s efforts are reinforced through joint initiatives under the direction of Norwegian Oil and Gas and Konkraft, as well as authority initiatives such as Digital21 and OG21.

There has been considerable interest in exploration acreage on the Norwegian shelf, and a record-breaking number of production licenses were awarded in 2018 in both the ordinary licensing round and awards in predefined areas (APA). Exploration activity in 2018 has also been rising, with a total of 53 exploration wells, 17 more than in 2017. Estimates from the Norwegian Petroleum Directorate reveal that only close to half of the recoverable resources have been produced and sold so far. This shows that the Norwegian shelf is still attractive. This is confirmed by the fact that several new, medium-sized players have entered the Norwegian shelf in recent years as a result of mergers and acquisitions. Several of the major international oil companies have reduced their presence on the shelf through the sale of own and partner-operated licence shares, but the newcomers often see opportunities in these licences. These companies also contribute to a new dynamic by introducing different forms of cooperation and business models.

Summary of SDFI results

Cash flow to the state was NOK 120 billion in 2018, which is the highest cash flow in 5 years. The increase in relation to 2017 was NOK 33 billion, mainly due to significantly higher oil and gas prices.

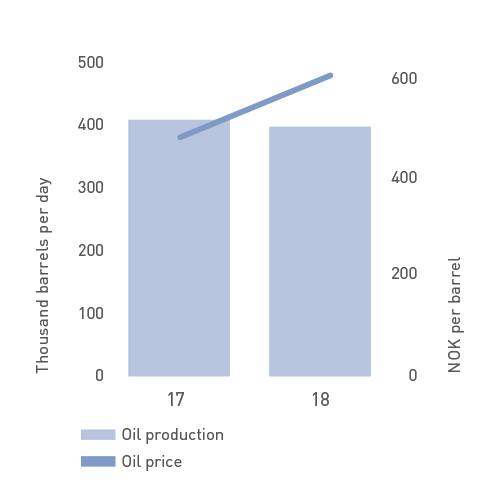

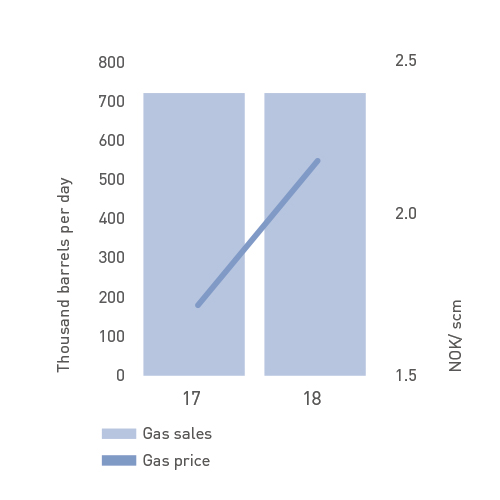

Total production was 1.085 million barrels of oil equivalent (o.e.) per day, just above 2 per cent lower than in 2017. Gas production was at a record-high level in 2018, marginally higher than in 2017. Together with high gas prices, this resulted in gas revenues from own produced gas of nearly NOK 90 billion.

Liquid production was 372 thousand bbl o.e. per day, 7 per cent lower than in 2017. The drop in liquid production is mainly caused by production shutdowns in connection with maintenance and natural production decline. In contrast to previous years, increase in number of wells on production efficiency has not compensated for the production decline. Nor were any new fields started up that contributed to production.

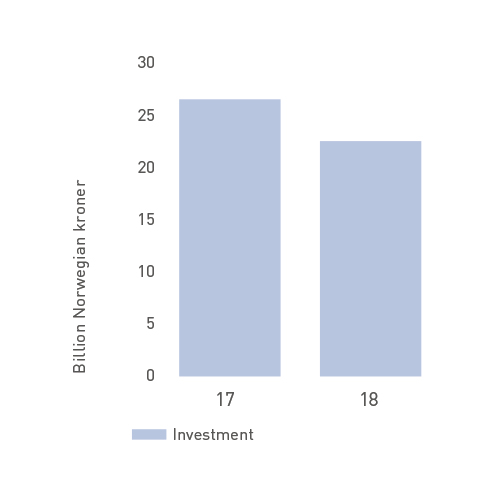

Investments in 2018 were NOK 23 billion, which is about NOK 3 billion lower than the previous year. The reduction is mainly due to drilling fewer wells, and a somewhat lower activity level within development.

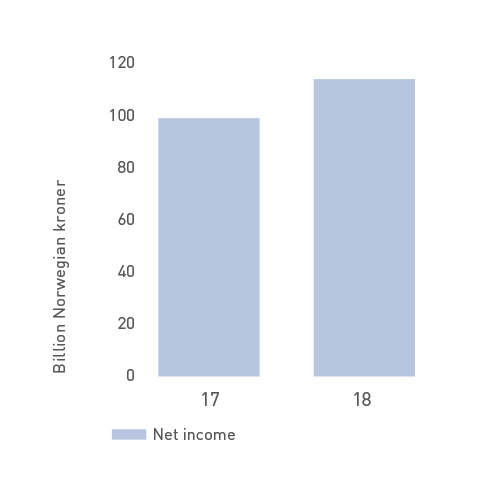

The annual profit in 2018 was NOK 114 billion, NOK 15 billion higher than in 2017. The increased profit as a result of higher prices was partly offset by impairment of the Maria field in 2018, reversal of previous years’ impairments in 2017, as well as change in loss provisions for outstanding positions in the gas market and recognition of liability for the negative outcome of the initial verdict from the District Court in the case of Troll Unit.

The positive trend of reduction in production costs has reversed, and costs increased in 2018. Cost must therefore be carefully monitored in the time ahead.

Recorded assets were NOK 247 billion at 31 December 2018. The assets consist of fixed assets related to field installations, pipelines and onshore facilities, as well as short-term debtors. Equity at year-end was NOK 163 billion.

Main activities in 2018

At the end of 2018, the portfolio consisted of 198 ownership interests in production licences, 12 more than at the beginning of the year. In January 2018, the Ministry of Petroleum and Energy implemented awards in predefined areas (APA 2017) where 17 production licences were awarded with SDFI participation. In the 24th licensing round in June 2018, 6 production licences were awarded with SDFI participation. During the course of 2018, 2 production licences were carved out from existing licences, 11 production licences were relinquished and 2 were sold. In January 2019, the Ministry of Petroleum and Energy implemented APA 2018, where an additional 14 production licences were awarded with SDFI participation.

In 2018, plans for development and operation (PDOs) were submitted for Johan Sverdrup phase 2 and for Troll phase 3. During the course of the year, the authorities approved the PDOs for Johan Castberg, Snorre Expansion Project and Troll phase 3. The third phase in the Troll development realises 2.2 billion bbl o.e., has a break-even price under 10 dollars per barrel and a CO2 intensity of 0.1 kg per bbl.

Production from the mature oil fields continues to dominate liquid production in the SDFI portfolio. The Troll, Oseberg, Åsgard, Heidrun, Grane, Snorre and Gullfaks fields accounted for 68 per cent of the total liquid production in 2018. The gas share of total production measured in o.e. amounted to 66 per cent in 2018. More than 72 per cent of the gas production came from the Troll, Ormen Lange and Åsgard fields. No new fields came on stream in 2018, but two new further development projects on existing fields, Oseberg Vestflanken 2 and Visund Nord IOR, started production in 2018. The Polarled pipeline also started operations, initially to route gas from Aasta Hansteen to Nyhamna. Polarled lays the foundation for new activity in the Norwegian Sea.

The company’s strategy was updated in the first half of 2018 and has three strategic areas: Competitiveness, Mature fields and Wells. These areas are supported by four strategic prioritisations: Well maturation and drilling efficiency, Optimised recovery strategy, Fields and further development, and Effective operations. A common factor for all these prioritisations is to exploit the opportunities created by the work on digitalisation. Through focussed follow-up supported by in-depth technical efforts, Petoro works to reinforce value creation opportunities with emphasis on long-term business development. The company’s climate policy emphasises that Petoro shall contribute to making the oil and gas industry on the Norwegian shelf a leader in meeting the climate challenges.

In line with this strategy, Petoro has devoted particular efforts to the Troll, Heidrun, Oseberg and Snøhvit fields in 2018. Well maturation and digitalisation have also been addressed as special topics for the entire field portfolio.

On Troll, where Petoro has an ownership interest of 56 per cent, the company has worked for several years to shed light on the consequences that increased gas production can have on the oil production. The development of digital technologies has dramatically accelerated the pace of data handling. Through close cooperation with the service provider, Petoro has applied “next generation” reservoir simulation tools on Troll, where the reservoir model and pipeline system on the seabed were joined in a comprehensive model to analyse the link between oil and gas production from the field. The results from these studies also contributed to support the preparation of the PDO for Troll phase 3, as well as the licence’s annual application for gas export volume.

On Heidrun, where Petoro has an ownership interest of 57.7 per cent, the company has conducted its own simulation studies in 2018 aimed at optimising the drainage strategy and contributing to identify new drilling targets. This effort has supported the work on Heidrun redevelopment and the approved lifetime extension for the field. This could realise significant value through the Heidrun nord phase 2 project. Petoro’s efforts over several years have been important for the development and results on the field, and illustrate the value of diversity among the licensees in a licence with a view towards arriving at good, comprehensive solutions.

On Oseberg, where Petoro has an ownership interest of 33.6 per cent, the company has conducted its own simulation studies in 2018 for the southern part of Oseberg to identify the potential for new improved oil recovery measures on the field. This work has contributed to identify new drilling targets that can be drilled from existing infrastructure on the field, and which therefore have both low investment costs and risk.

On Snøhvit, where Petoro has an ownership interest of 30 per cent, the company has had significant preparatory work in 2018 aimed at the investment decision for the Askeladd project, which will be the first plateau extension of the field since its start-up in 2007. Among other things, Petoro has addressed the rig strategy, synergies with other fields in the area and subsurface work. The investment decision was made in 2018.

As regards new fields in the portfolio, Petoro’s efforts in 2018 have included preparations for the investment decision and the PDO for Johan Sverdrup phase 2, where Petoro has an ownership interest of 17.36 per cent. The PDO was submitted to the authorities in August. Johan Sverdrup is a pioneer field within digitalisation. Here, Petoro has been involved in the licence’s work to make a decision on full coverage of the field with seismic cables for reservoir monitoring, implementation of fibre optics in wells, along with installation of equipment for water and gas injection (WAG). These decisions are expected to contribute to significant improved recovery.

Establishment of a solution for power from land to Johan Sverdrup and the other fields on the Utsira High is also part of phase 2. The Johan Sverdrup project has also experienced positive cost development in 2018, and the project distinguishes itself with its good profitability.

Over the course of 2018, Grane and Åsgard started a joint centre for integrated operations. The centre monitors and supports offshore operations from land. This is an example of digitalisation which, through easier access to data, specialised software and changes in the operations model, enables better utilisation of the facilities’ capacity, optimisation of energy consumption and improved safety. The plan is to expand to include more fields and new centres.

Petoro has followed up a large portfolio of new, major development projects in 2018: Johan Sverdrup phase 1, Johan Castberg, Snorre Expansion Project, Martin Linge and Dvalin.

The follow-up work has targeted several factors that have an impact on HSE, climate and implementation risk, and has also focussed on ensuring good preparations for operation.

Subsea wells account for about 60 per cent of the SDFI production. In contrast to the positive development in drilling pace for new wells from fixed installations in recent years, updated forecasts reveal a need to increase the number of new subsea wells on mature fields in the years to come. In an effort to increase the scope of subsea wells in the SDFI portfolio and supplement efforts by operators, Petoro has worked in 2018 to mature proposals for new well targets on selected fields with significant subsea infrastructure, such as Oseberg and Gullfaks. This work also contributes to efficient utilisation of rig capacity.

Over the course of 2018 there has been increased activity in Petoro’s portfolio linked to electrification measures that can contribute to substantial reductions in greenhouse gas emissions from the SDFI portfolio, also for the mature fields. On several fields, such as Troll, Snorre and Gullfaks, project development is underway with a view towards decisions within the next few years. If these projects are realised, they could contribute a reduction in CO2 emissions of nearly 2 million tonnes per year on the Norwegian shelf, corresponding to 0.8 million tonnes per year for SDFI. The first investment decision is expected in 2019 and is in regard to the floating wind turbine facility in the Tampen area, that will partially electrify Snorre and Gullfaks.

Petoro participated in 17 exploration wells in 2018, of which ten were wildcat wells that resulted in 6 new discoveries. Four of these are gas discoveries, and the most promising of these is Balderbrå in the Norwegian Sea. One new oil discovery was also made, Skruis in the Barents Sea. This is situated close to existing infrastructure and will be evaluated with a view toward tie-in to Johan Castberg. Appraisal of the Cape Vulture discovery in the Norwegian Sea was successful. Presuming a positive development decision, this will mean a doubling of remaining oil reserves that can be produced through the Norne field. Appraisal of the Grosbeak discovery in the North Sea also yielded a positive result, and further plans for developing the field are being assessed.

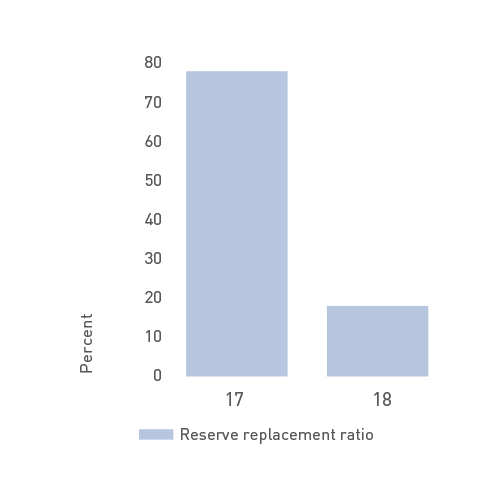

At the end of 2018, the portfolio’s expected remaining oil, condensate, NGL and gas reserves were 5 545 million bbl o.e., a decline of 334 million bbl o.e. compared with the end of 2017. The growth in reserves of 62 million bbl o.e. was considerably lower than production in 2018, which was 396 million bbl o.e. The reserve replacement rate was 16%. Reserve growth in 2018 primarily came from the decision on Johan Sverdrup phase 2.