Petoro manages the State’s Direct Financial Interest (SDFI), which represents about a third of Norway’s total oil and gas reserves. The company’s principal objective is to create the highest possible financial value from this portfolio.

The SDFI was established with effect from 1985. Under this arrangement, the state participates as a direct investor in petroleum operations on the Norwegian continental shelf (NCS) so that the Treasury receives revenues and meets expenses associated with the SDFI’s participatory interests directly and outside the regular system for taxing petroleum revenues. Petoro acts as the licensee for the state’s participatory interests in production licences, fields, pipelines and land-based facilities, and manages the SDFI on the basis of sound business principles.

Summary of SDFI results

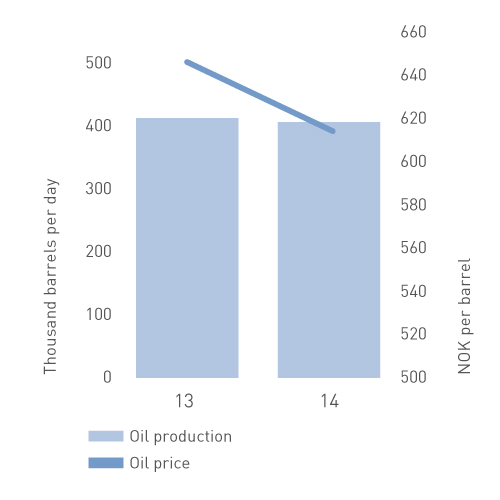

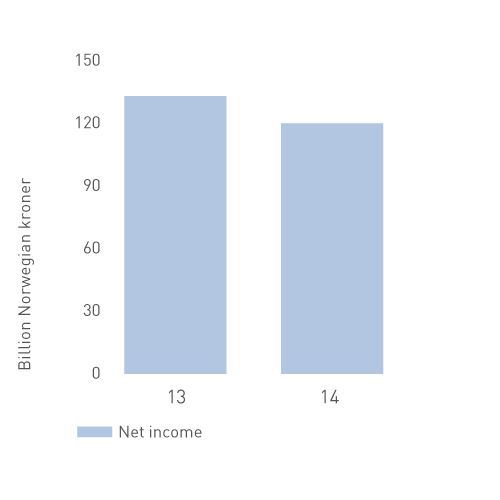

Net income in 2014 came to NOK 119.7 billion, compared with NOK 132.8 billion the year before. This result was affected by the development of oil and gas prices, and yielded a cash flow to the government of NOK 111.1 billion as against NOK 124.8 billion the year before. Total production averaged one million barrels of oil equivalent per day (boe/d), about three per cent lower than the 2013 figure. Sales for the year corresponded to production.

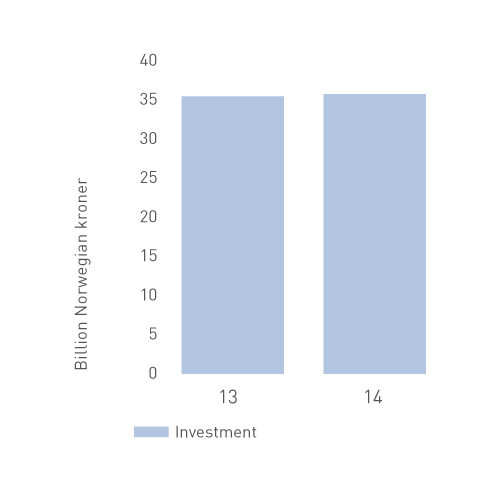

Investment for 2014 totalled NOK 35.7 billion, which was on a par with the year before.

At 31 December 2014, the portfolio’s expected remaining oil, condensate, NGL and gas reserves comprised 6 145 million boe. That was down by 277 million boe from the end of 2013 when account is taken of production for the year and new reserves.

The book value of assets totalled NOK 265.6 billion at 31 December 2014. These assets mainly comprise operating facilities related to field installations, pipelines and land-based plants, as well as current debtors. Equity at 31 December amounted to NOK 171.5 billion. Future removal-liabilities are estimated at NOK 77.5 billion. Current liabilities, which comprise provision for costs incurred but not paid, were NOK 14.1 billion at 31 December.

An external valuation was also conducted by the Ministry of Petroleum and Energy in 2014, which estimated the value of the SDFI portfolio to be NOK 1 234 billion at 1 January 2014.

External trends

Global economic growth was weaker than expected in 2014 and helped to curb the increase in demand for oil. At the same time, oil production from non-Opec countries – particularly shale oil output in the USA – maintained strong growth. A deterioration of the balance between supply and demand in the market and Opec’s decision in November to refrain from adjusting its production to help redress that balance resulted in a sharp fall in the price of oil. Brent Blend was down to USD 55 per barrel at 31 December 2014, less than half its peak of USD 115 in June. The average price achieved by the SDFI portfolio in 2014 was USD 99 per barrel, compared with USD 110 the year before. A strong US dollar meant that the reduction was not quite as steep measured in Norwegian kroner. The average price in the latter currency was NOK 617 per barrel, down NOK 30 from 2013.

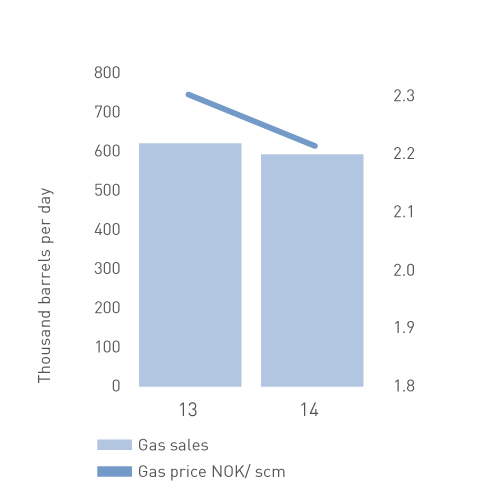

The declining trend in European demand for gas continued in 2014. Weak economic growth, competition from renewable energy and coal, and a mild winter were the main reasons for this development. European imports of liquefied natural gas (LNG) were on a par with 2013. Russian gas deliveries to Europe were somewhat lower than the year before, while exports of Norwegian gas remained at the same level. Gas exports from the SDFI portfolio were somewhat lower than originally planned, primarily because some production was deferred to boost its value. High stocks at the start of the summer season and robust supplies weakened gas prices during the year. The average gas price achieved for the SDFI portfolio was NOK 2.23 per standard cubic metre (scm), compared with NOK 2.31 in 2013.

Costs have risen sharply over the past decade in all parts of the industry, including field development, operation and maintenance, modification projects, subsea developments and drilling. The increase has been general at all levels of the supply chain. Agreement prevails in the industry that this trend is unsustainable.

Big oil companies have changed their commercial goals during 2013-14 from volume growth towards financial parameters such as cash flow and dividend. That has meant stricter prioritisation of investment funds and increased profitability requirements for new projects. The outcome is that projects are being halted, postponed or continued with a reduced scope.

A substantial commitment was made in 2014 to enhancing efficiency and reducing the level of costs on the NCS. Efficiency improvement efforts currently under way involve all parts of the value chain. Operators and the other licensees have individual approaches to this work.

Portfolio transactions on the NCS have increased in scope during recent years. This has been driven particularly by the individual company’s need to free up cash, as manifested through the sale of participatory interests with investment commitments. Portfolio transactions are also used to realise strategic goals and improve tax positions. The interest in selling out of licences is somewhat higher than the availability of relevant buyers. Petoro has so far not found it relevant to exercise the pre-emptive right it holds with respect to all sales of participatory interests in joint ventures on the NCS.

Exploration activity on the NCS was at a high level in 2014. Fifty-nine exploration wells were completed, unchanged from the year before. A record number of exploration wells were drilled in the Barents Sea – 14 compared with 10 in 2013. Exploration activity in this area resulted in a couple of very interesting oil discoveries and successful appraisals. But exploration results in recent years have failed to meet the earlier optimistic estimates, and coming up with profitable development solutions is a challenge.

Attention in petroleum activities on the far northern NCS has shifted from the Snøhvit area, gas resources and gas infrastructure to oil resources in discoveries such as Johan Castberg and Wisting.

The international debate on climate change has continued to challenge the role of fossil fuels in the future global energy mix. A greater concentration on the environment and the climate will be significant with regard not only to demand and prices for oil and not least for gas, but also to the industry’s commitment and choices related to improved recovery and new field developments.

Health, safety and the environment (HSE)

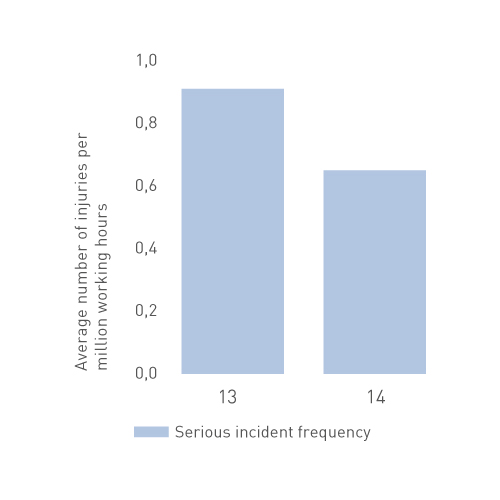

The improvement in HSE results is continuing. No incidents with a major accident potential occurred in 2014. Nor were there any large individual discharges to the sea or on land. The serious incident frequency has been developing positively for a number of years, and came to 0.7 per million working hours in 2014 compared with 0.9 the year before. The personal injury frequency also made progress, falling from 4.4 in 2013 to 3.8.

Major restructuring and change processes in the industry are influencing the risk picture, and Petoro has become more vigilant over HSE and technical integrity in its follow-up of licences.

An initiative was taken by Petoro, ConocoPhillips, ExxonMobil and Total in 2010 to improve the involvement of licensees in safety efforts. This work led in 2014 to guidelines for handling major accident risk at licence level, which has resulted in increased involvement by licensees in risk management. These guidelines are now being incorporated as an industry standard through the Norwegian Oil and Gas Association. Petoro participated during 2014 in 11 working meetings on major accidents, and the experience was positive. It also participated in several HSE management inspections on selected fields and installations during the year.

Highlights and results 2014

The SDFI portfolio comprised 182 production licences at 31 December, up by three from 1 January. Participatory interests in 11 production licences were awarded for Petoro to manage during January 2015.

Following a revision of the company’s strategy in 2013, its attention is concentrated primarily on mature fields, field development and the far north. An assessment in the autumn of 2014 determined that this strategy continued to provide the right response to the challenges and opportunities facing Petoro.

Output from the mature oil fields continues to dominate production in the SDFI portfolio. Troll, Åsgard, Oseberg, Heidrun, Snorre and Gullfaks accounted for about 60 per cent of total liquids production, while 75 per cent of gas output came from Troll, Ormen Lange and Åsgard. Only limited new capacity was introduced in 2014 when production began from the fast-track projects Fram H-North and Svalin C and M in the North Sea. Valemon and Eldfisk II came on stream in early January 2015. Huldra ceased production in the autumn of 2014.

In line with the strategy, work continued in 2014 on realising the reserve base and supplementary resources in the mature fields. Special commitments were made with Snorre, Heidrun and Oseberg. Petoro has given particular emphasis to realising greater drilling efficiency on these fields and to clarifying their reserve and resource bases.

Petoro continued to be active as a driving force for the Snorre 2040 project, and contributed through its own work to strengthening the reserve base and development solution for a possible new Snorre C platform. These efforts have led to a positive development of reserves which could be developed with such an installation. On the development side, Petoro has proposed a number of specific measures to reduce the weight and thereby the cost of a new platform. A decision on continuation (DG2) has been postponed several times and was scheduled in February 2015 for the fourth quarter of 2016. Plans now call for an investment decision in 2017, with production starting in 2022. This postponement reflects unsatisfactory profitability for the project, and work is now under way on more thorough changes to the platform solution. The choice of concept remains unchanged. Petoro has been concerned that the project is time critical. A delay to the timetable for such a development involves the risk of losing reserves because of the limited technical operating life of existing installations. Further work will include a closer look at measures which can counteract this.

Through its own independent work on understanding the reservoir in 2014, Petoro identified an increased reserve base in Heidrun and the associated need for additional well targets on this field. This contributed to a decision by the partnership to continue with a binding process for deciding on a Heidrun future development project. Conceptual studies will address the whole resource potential of this field, and a choice of concept is planned for late 2016.

The contribution made by Petoro to the Oseberg future development project led to the identification of a reserve base which meant that a simple new unstaffed wellhead platform was chosen as the concept, in line with the company’s wishes.

Petoro’s commitment to Johan Sverdrup in 2014 concentrated particularly on promoting an integrated development of the field both in the first phase and for subsequent stages. The company has worked on solutions which ensure maximum long-term value creation, including one field centre, robust power capacity and provision for measures which can improve recovery. The concept chosen in February 2014 for phase one was in line with Petoro’s view. The company has conducted extensive analyses of the potential for enhanced oil recovery (EOR), and proposed solutions for this. Combined with other promising measures for improved recovery in the future, that potential will be studied further as an integrated part of work on phase two leading up to the choice of concept in 2016. This is in line with Petoro’s strategy of safeguarding future opportunities when pursuing new field developments.

The company actively supported Statoil’s candidacy to serve as operator for the unitised field. This proposal received unanimous support from the partnership in the fourth quarter of 2014.

Petoro completed its own evaluations during the year as the basis for securing a rightful share of the value in this large field, which extends over several licences with a different composition of partners in each licence. The supplementary appropriation from the owner for this purpose was increased in 2014, tailored to the applicable plans for the Johan Sverdrup project. Extensive unitisation negotiations were conducted throughout 2014 and right up to the submission of the plan for development and operation (PDO) to the government on 13 February 2015. At that point, a majority of the licensees in the underlying licences – including Petoro – expressed support for a unitisation agreement which was submitted to the government for final determination of its terms.

In the far north, Petoro’s attention has been concentrated on measures for improving regularity in Snøhvit LNG and efforts to ensure that all relevant development solutions for the Johan Castberg field are matured and assessed ahead of a final concept choice. Production efficiency for Snøhvit LNG came to 84 per cent, including turnarounds, which encourages expectations that plant and operating problems experienced over a number of years have been overcome. Work on the choice of concept for Johan Castberg continued throughout 2014. Petoro has been concerned to ensure that the various development solutions are individually optimised while also increasing their robustness to profitability challenges and uncertainties in both short- and long-term perspectives.

Petoro continued to direct the industry’s attention during 2014 towards the need for efficiency enhancements and cost reductions, particularly in the drilling and well service area. As the dominant operator in the SDFI portfolio, Statoil achieved good results with a number of individual wells during the year.

Increasing attention was paid by Petoro in 2014 to the need for improved efficiency in development, operation and maintenance as well. The company has worked to ensure that the measures adopted are sustainable in both short and long terms, and involve a genuine enhancement in efficiency rather than simply a reduction in activity. The aim is to secure the profitability of investment in mature fields and new developments. Petoro saw in 2014 that the trend towards rising field costs had reversed. Restructuring efforts by the operators also contributed to some reduction in operational modifications. Operator improvement measures are expected to yield greater effects in the longer term.

Only one PDO was submitted to the government in 2014, covering Gullfaks Rimfaksdalen where the SDFI is a participant. The PDO for Flyndre was submitted in 2013 and approved by the government in 2014.

Petoro participated in 20 of the 59 exploration wells completed on the NCS in 2014, and in 10 of the 22 discoveries made.

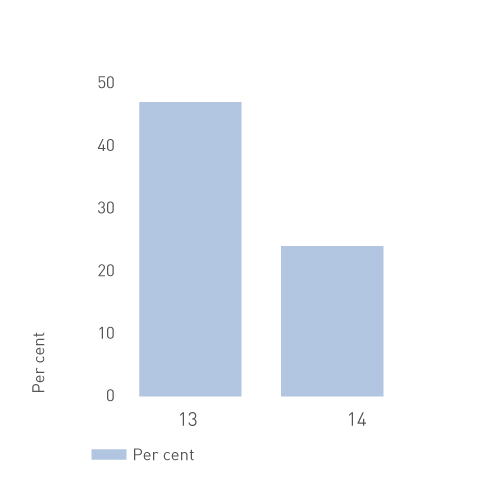

Reserves showed a net increase of 88 million barrels of oil equivalent (boe) during the year. This figure was low because few decisions were taken in 2014 to invest in new developments and improved recovery measures on existing fields in the SDFI portfolio. Most of the increase reflected a more uniform reporting of reserves for new wells on fields operated by Statoil. Reserves were also downgraded on some fields. A total of 365 million boe was produced in 2014, giving a net reserve replacement rate of 24 per cent. The comparable figure in 2013 was 47 per cent.