Petoro manages the State’s Direct Financial Interest (SDFI), which represents about a third of Norway’s total oil and gas reserves. The company’s principal objective is to create the highest possible financial value from the SDFI portfolio.

The SDFI scheme was established in 1985. Under this arrangement, the state participates as a direct investor in petroleum activities on the Norwegian continental shelf (NCS), so that the state receives revenues and meets expenses associated with SDFI’s ownership interests. Petoro acts as licensee for the state’s ownership interests in production licences, fields, pipelines and onshore facilities, and manages this portfolio based on sound business principles. As SDFI manager, Petoro contributed a cash flow of NOK 87 billion in 2017, which represents a significant portion of the state’s total revenues from the petroleum activities.

External trends

The last few years have seen considerable changes in the oil and gas industry, including on the Norwegian shelf. Low prices and increased uncertainty as regards supply and demand for oil and gas over the longer term have clarified the need for efficiency and adjustments. In this situation, the industry and players have been able to considerably reduce costs over a relatively short period of time, thus bolstering competitiveness on the Norwegian continental shelf. 2017 was the first year since the financial crisis where the economy grew on all continents. Heading into 2018, the key financial figures are better than has been the case for a number of years, and the overall global financial growth was a positive surprise in 2017 with a total of 3.7 per cent.

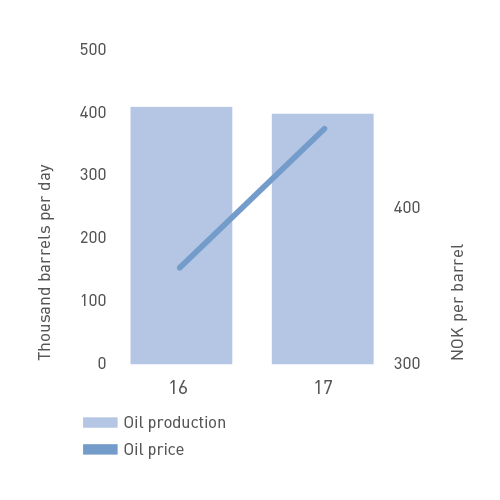

After a period of oversupply, the oil market rebalanced over the course of 2017. This is bolstered by broad growth in global demand, which at 1.8 million bbls per day, was the strongest since 2010. On the supply side, OPEC continued the reduction agreement of 1.2 million bbls per day throughout year, and the decision was made in November 2017 to continue this through 2018. US shale oil production is growing again, and the scope of shale oil, alongside geopolitical unrest in the Middle East, are key uncertainty factors for future oil price development. The year started off with an oil price around USD 55 per bbl, but this declined steadily toward the summer and reached a low for the year at USD 44 per bbl in mid-June. The price rebounded over the course of the year and ended the year at USD 66 per bbl. SDFI’s average realised oil price was NOK 449 per bbl, NOK 88 higher than in 2016. Measured in USD per bbl, the average price in 2017 was 54.2, compared with 43.1 in 2016.

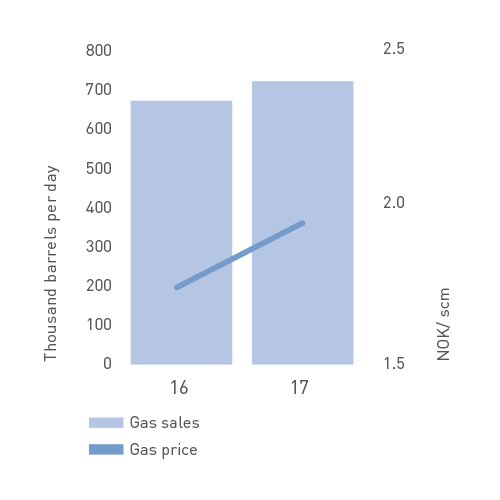

European demand for gas continued its positive development from 2016 and grew by about 5 per cent in 2017. Some of the growth is attributed to factors such as colder and drier weather conditions in Europe. However, there has also been more structural growth in demand from the power sector driven by higher coal prices and the phasing out of coal power plants. While both Norwegian and Russian gas exports to Europe reached new record levels in 2017, LNG imports also reached their highest level of the last 5 years. This reflects a decline in Europe’s own production which, combined with production restrictions on the Groningen field, increased Europe’s need for imports. In 2017, gas prices declined seasonally toward the summer and rebounded significantly toward the winter. The average gas price achieved for the portfolio was NOK 1.72 per scm in 2016, compared with NOK 1.62 per scm in 2016.

The Paris Climate Agreement appears to be strong, even after the US decision to withdraw from the agreement. Implementation of the Paris Agreement is challenging for several countries, which is particularly demonstrated by the discussions in the EU and several member states. Germany has taken a leadership role as regards climate and renewable energy, but will most likely not reach its climate goals for 2020. In the UK, renewable energy and gas have replaced coal and contributed to considerable emission reductions. Further reductions will require substantial and costly efforts within transport and heating. Despite various challenges, the long-term goals and ambitions remain firm.

The Norwegian petroleum industry has followed up the national climate goals by establishing a roadmap towards 2030 and 2050 for emission reductions. The goal is to implement CO2-reducing measures corresponding to 2.5 million tonnes per year from 2020 to 2030 through low-emission solutions in new projects and energy efficiency measures in existing facilities.

The situation with increased uncertainty in future product prices requires financial robustness as regards investment decisions. This means that measures to develop new and existing petroleum deposits are shifted towards projects with lower break-even prices, shorter repayment periods and phased development.

The player landscape on the Norwegian shelf is changing. 2017 saw a continuation of the trend where large international oil companies are reducing their presence, including through the sale of self-operated fields. Industry consolidation through mergers and acquisitions has also included the European industrial and energy companies that, for several years, have strengthened their presence on the Norwegian shelf in both in the development and operations phase. The changes have allowed the small and medium-sized independent oil companies to grow in terms of both size and financial strength. The players that grew in 2017 are primarily financed by Private Equity funds or large industrial players. So far, the industry consolidation and restructuring has not affected operatorships and has only somewhat affected the composition of partnerships in Petoro’s producing fields. However, participants in production licences with SDFI participation have been affected, either through mergers and the establishment of larger companies or in that the companies have sold their self-operated activity and associated organisation. Further efficiency and cost improvement measures, in addition to high exploration activity and new discoveries, will be decisive in order for the Norwegian shelf to maintain its competitiveness in the global competition for investment funds.

Although there has been a decline in the number of exploration wells over the last few years, the number of applications and awards in the last licensing rounds show that there is still interest in exploration on the Norwegian shelf. The 2016 Awards in Predefined Areas (APA) totalled 56 production licences, while the 2017 APA set a new record with 75 licenses.

Over the last three years, the industry and players have demonstrated a sound ability to improve, and the challenge moving forward is to maintain the effect of this and, at the same time, have the capacity for further improvement.

An effort was under way in 2017 under the auspices of Konkraft with the aim of promoting global competitiveness for Norwegian oil and gas over the long term. The report was submitted on 4 January 2018, and the committee points out opportunities for improvement, particularly within digitisation and new forms of cooperation. It is important for the industry to follow up and implement these measures in the time ahead.

Summary of SDFI results

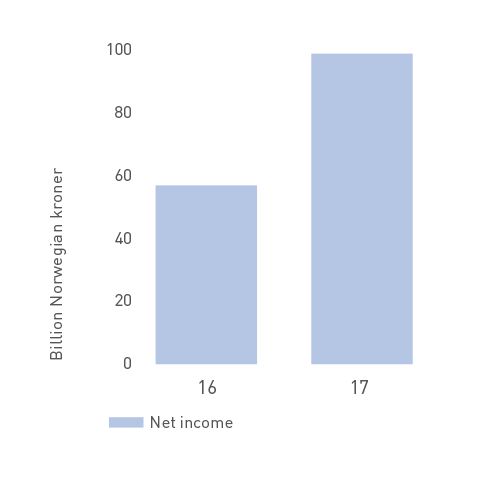

The financial result for 2017 was a net income of NOK 99 billion, NOK 41.5 billion higher than in 2016. Cash flow to the state was NOK 87 billion in 2017, NOK 21 billion higher than in 2016.

The cash flow and financial result are characterised by considerably higher oil and gas prices in 2017 compared with 2016, as well as higher gas volumes. Total production averaged 1.110 million barrels of oil equivalent (boe) per day, up roughly seven per cent from 2016. Gas production reached a record level in 2017, 13 per cent higher than in 2016. The increase is primarily due to increased use of flexible gas production in order to exploit higher prices. Natural production decline from existing wells means that liquids production was nearly three per cent lower than in 2016. Higher regularity and more wells do not fully offset this decline, as has been the case over the last couple of years.

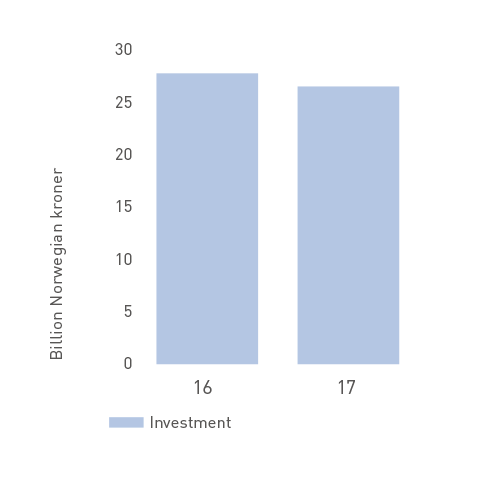

Costs incurred for investment in 2017 totalled NOK 25.5 billion, which is about NOK 3 billion lower than the year before. This reduction is mainly due to lower investment in production drilling as a result of reduced drilling activity on three fields.

The book value of assets at 31 December 2017 was NOK 247 billion. The assets consist of fixed assets related to field installations, pipelines and onshore plants, as well as current debtors. Equity at 31 December came to NOK 168 billion.

Health, safety and the environment (HSE)

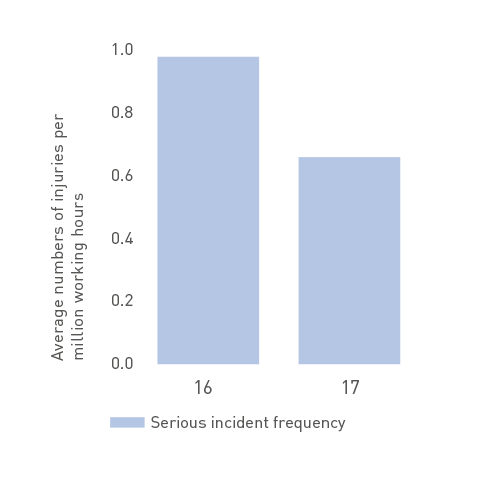

The HSE results for 2017 show a positive development compared with the previous year, but the number of serious near-miss incidents and personal injuries is still too high. The serious incident frequency (number of serious incidents per million hours worked) declined from 1.0 in 2016 to 0.7 in 2017. The personal injury frequency (number of personal injuries per million hours worked) is at same level as the previous year and came to 4.2 in 2017, compared with 4.1 in 2016. No serious discharges to sea were recorded in 2017.

In 2017, Petoro has been particularly concerned with risk assessments in a major accident perspective linked to effects from efficiency measures in the licenses. Petoro also conducted a number of management visits in 2017, focusing on health, safety and the environment on selected fields and onshore plants.

Beyond the activities on the Norwegian shelf, Petoro, as licensee in the Martin Linge project, experienced the tragic accident at the Samsung shipyard in South Korea on 1 May 2017, where 6 people lost their lives and 25 were injured. This accident is a powerful reminder of the importance of managing major accident risk linked to all parts of our activities.

Principal activities in 2017

As of the end of 2017, the portfolio consisted of 186 production licences, 6 more than at the beginning of the year. In January 2017, Petoro received participating interests in 13 production licences under the Awards in Predefined Areas (APA) 2016. Petoro also received participating interests in 17 production licences in APA 2017 in January 2018.

Production from mature oil fields continues to dominate liquids production in the SDFI portfolio. The Troll, Oseberg, Åsgard, Heidrun, Grane, Gullfaks and Snorre fields accounted for 70 per cent of total liquids production in 2017. In 2017, gas accounted for 64 per cent of overall production measured in oil equivalent. Just over 70 per cent of gas output came from Troll, Ormen Lange and Åsgard. Three new fields came on stream in 2017: Maria, Sindre and Flyndre. Maria started up in December, nearly one year before the original schedule and development costs were considerably lower than presumed in the Plan for Development and Operation (PDO).

The company’s strategy was continued in 2017 and is twofold: Increase the competitiveness of the portfolio and realise value in mature fields. Through focused follow-up, supported by in-depth professional commitment, Petoro works to reinforce value creation opportunities with emphasis on long-term business development. The company’s climate policy emphasises that Petoro shall contribute to ensure that the oil and gas industry on the Norwegian shelf is at the forefront as regards addressing the climate challenges. In this area, the company has focused its efforts on energy efficiency measures on the fields in the portfolio with the highest CO2 emissions.

In 2017, in line with the strategy to realise the values in mature fields, particular efforts have been aimed at the Snorre and Troll fields, in addition to well maturation on selected fields.

On the Snorre field, Petoro has been an active driving force over a number of years in the realisation of additional profitable reserves. Efforts have primarily been aimed at strengthening reserve potential through expansive technical reservoir studies. In December 2017, the license decided to invest in a further development project consisting of 6 seabed templates adapted for 24 new wells. The application for approval of the amended PDO for further development of the Snorre field was submitted to the Ministry of Petroleum and Energy in December. Production start-up is anticipated in 2021, and the project will contribute to considerably increased values from the Snorre field.

The Troll field is facing important decisions as regards further development of the field. Throughout 2016 and 2017, Petoro has been actively engaged in helping ensure that work on the Troll phase 3 project will ensure the most comprehensive and flexible further development possible. Efforts have primarily been aimed at ensuring that the effect on oil production is understood through comprehensive technical reservoir studies. An investment decision is expected in spring 2018, and start-up in 2021.

On the Heidrun field, Petoro has also been carrying out technical reservoir studies over a longer period of time in order to contribute toward improving the profitability of further development measures. In 2017, the license made an investment decision for phase 1 of the Heidrun Subsea Extension project. This project includes construction of a new production flowline and an upgrade of subsea equipment in the northern part of the field. This will enable the drilling of 11 new wells, which will yield considerably greater values from Heidrun.

In December 2017, along with the other partners in the Johan Castberg license, Petoro made an investment decision and subsequently submitted the application for approval of the PDO for the Johan Castberg project, which comprises 10 seabed templates, two satellites and one production vessel. This project has undergone extensive changes and cost improvement measures, where Petoro has been particularly focused on preserving the opportunities for new profitable additional volumes in the field’s operations phase. The change work carried out by the operator Statoil along with the suppliers has yielded very good results and has resulted in a substantial improvement in the project’s profitability.

Petoro is highly involved as a partner in the Johan Sverdrup field, where phase 1 of the project is in the implementation phase with two platforms under construction in South Korea and two in Norway. A dedicated facility is also being constructed at Kårstø to supply the field with power from shore.

In addition to following up the implementation of phase 1, Petoro has been involved in preparations for the investment decision in 2018 for phase 2 of the project. Johan Sverdrup has also experienced a positive cost development in 2017, which helps boost the project’s profitability.

The authorities approved the PDO for the Dvalin field in 2017. The development plan for Dvalin comprises a subsea template with four wells tied into the Heidrun platform, as well as gas export via Polarled and Nyhamna. Petoro is also a licensee on Ekofisk, where the authorities approved an amended PDO in 2017 for the Ekofisk South Water Injection project. The objective of the project is increased recovery through the installation of a new subsea template with four water injection wells.

The need for efficiency improvements and cost reductions within the drilling and well service area has been an important issue for Petoro over several years. Petoro has followed the development in drilling pace on ten fixed installations on five selected fields in the portfolio over a number of years. The number of completed wells has doubled from 2014 to 2017. The average drilling time and drilling cost was cut in half from 2014 to 2015. The result can mainly be attributed to increased drilling efficiency, simplified well design and increased availability of drilling facilities. The development in drilling time and drilling cost has levelled out since 2015, and was on par with the previous two years in 2017. Further improvements will require new means, e.g. digitisation and new forms of cooperation.

There will be a significant long-term need for drilling new wells to realise the value potential in mature fields. Petoro has been working to increase the maturation of wells on selected fields, in part by carrying out in-depth studies to identify new wells.

As part of this strategy, Petoro has worked to increase the portfolio’s competitiveness, and the licenses have achieved comprehensive improvements within all areas of the value chain. The substantial cost reductions achieved through optimisation of the development concepts leading up to concept choice for Snorre and Johan Castberg, were decisive as regards the projects’ profitability and being able to make investment decisions in 2017. Even with reduced costs, the recoverable resources have been maintained for these projects, which demonstrates a considerable improvement in competitiveness. These experiences provide a sound basis for maturing new profitable projects in the portfolio.

Another example of results from the improvement efforts is that field costs for fields in operation are still declining. However, after achieving substantial cost reductions in recent years, the effect has slowed down, and field costs in 2017 were four per cent lower than in 2016. Further reductions here will also require new measures. Petoro’s efforts have been aimed at ensuring that the measures implemented to reduce costs are sustainable and entail an actual gain in efficiency, without weakening the facilities’ integrity over the longer term.

34 exploration wells were completed on the Norwegian shelf in 2017, which is about the same number as the year before. Petoro was a participant in 12 of the wells, 10 of which were wildcat wells that yielded 8 new discoveries. The last two exploration wells were appraisal wells. Even though the new discoveries were generally minor, four of them are located near existing infrastructure and are presumed to be commercial. The results from the exploration campaign in the Barents Sea were disappointing, with the exception of the Kayak discovery where an additional appraisal well is considered with a view towards a potential development tied into Johan Castberg.

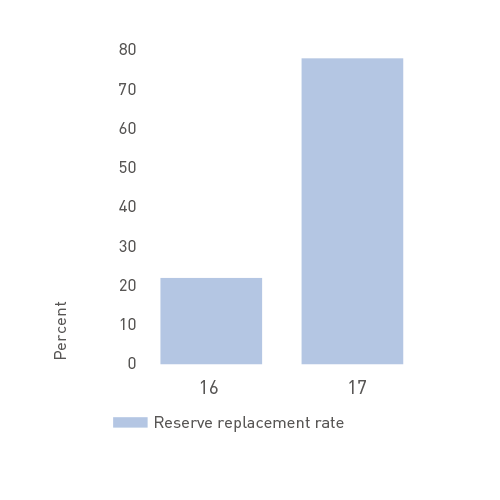

The portfolio’s estimated remaining reserves of oil, condensate, NGL and gas totalled 5879 million boe at 31 December, down by 89 million boe from the year before. Reserve growth in 2017 primarily came from Johan Castberg, but also from the mature fields Snorre, Åsgard, Heidrun, and Visund. Nevertheless, the growth was not sufficient to offset the reduction in remaining reserves from production in 2017.